Many people hitting their late 50s and early 60s today have well over $1 million in their 401(k) plans due to the tremendous stock market returns in the 80s and 90s. The S&P 500 returned over 1,100% from 1980 through 1999. That is a 14% annual return during this time period and a 10.3% real annual rate of return if we strip out inflation.

A 10.3% real rate of return over 20 years can do amazing things for a retirement portfolio. Let’s take a person who is 24 years old and has nothing saved in his 401(k) plan. Let’s say he starts saving $18,000 per year and his employer matches $5,000 per year for the next 20 years. In this scenario, our 24-year-old has well over $1 million in just 20 years.

The chart above shows just how powerful the compounding of returns can be over a long time period. In this case, 10.3% returns over 20 years are dramatic. At the same time, what gets lost on many people is just how quickly that ending figure can decline as we lower our annual rate of return assumption.

A Case Study In Compounding

To see how small changes in annual return assumptions can impact a person’s retirement plans, I put together a case study in our WealthTrace Retirement software. I took a 28-year-old couple that makes a combined $150,000 per year. They both max out contributions to their 401(k) plans at $18,500 each. Their employers match them $6,000 each. Currently, they have a total of $40,000 saved in their 401(k) plans.

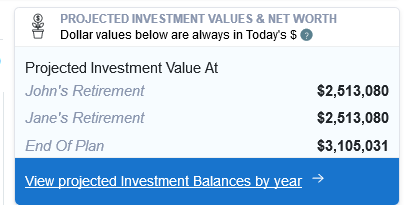

This couple is invested in 80% stocks and 20% long-term Treasury bonds. For their stock returns, I used long-term historical nominal returns of 7.9% per year. For bonds, I used a 3% annual return assumption. This gives them an average portfolio return of 6.9%. I ran their analysis and found the following:

In this retirement analysis, I set their retirement age to 65. What the above is telling us is that at age 65 they are projected to have around $2.5 million adjusted for inflation. At the end of their plan (their life expectancy of 87) they are projected to have around $3 million.

It’s simply amazing what a good 401(k) plan combined with saving diligently can do for a young couple. Of course, the 7.9% stock market return every year helps immensely too. Let’s see just how much this return assumption helps them.

I ran a few scenarios where the rate of return drops by 1%, 2%, and 3% on their retirement portfolio. The results can be seen below:

| Portfolio Value At Retirement | Portfolio Value At End Of Plan | |

| Base Case | $2.5 million | $3.1 million |

| Returns Down 1% | $2.0 million | $2.0 million |

| Returns Down 2% | $1.7 million | $1.3 million |

| Returns Down 3% | $1.4 million | $.79 million |

The decline in their investments is dramatic as we decrease their rate of return assumptions. A 3% decline in annual returns gives them $1.1 million less at retirement and $2.3 million less when they are 87 years old. This is a huge decline and shows why none of us should depend on 8% stock market returns forever. Making life-altering decisions based on these types of assumptions can set one up for a lot of pain in the future if these types of stock market returns don’t materialize.

Return Assumptions For Your Retirement Plan

As mentioned above, using 8% or higher returns on your stock portfolio forever is not a good idea. When figuring out how much you can withdraw from your portfolio over time, it’s best to be more conservative with expected returns. Otherwise, you might run out of money by age 75 and have to do something drastic, such as sell your home or move in with your kids. I recommend clipping 2% off the historical returns for stocks when putting in your return assumptions. And then if returns are better than this, you’ll have more money to spend in your later years and/or more money to leave to your heirs.